SAVING vs SPENDING: Will We Ever Be Prepared?

by Danielle Woods, daniellewoods@propel-fa.com

Did you know that writing your concerns down often helps to reduce the stress of worrying about them? Many of our clients worry about the future, but do not know how to get those worries on paper in a meaningful way. We strongly encourage clients to consider working with us to create a written FINANCIAL PLAN.

When I was 16 years old, I got my first real paycheck. Sure, I’d been doing family chores since age 7 and babysitting since age 10; but those earnings didn’t have the same impact as receiving an actual paper check and paying taxes like a real grown-up.

Before I’d even heard of a spreadsheet, I was drawing straight columns on my college-rule notebook paper and organizing my income and expenses in tidy little rows. I faithfully added to my savings account to buy a car when I was 17. I suppose it’s not that shocking that some years later I would choose to become a financial advisor. I know now that my vigilance over my finances is not something that comes naturally to everyone.

This month marks my 22nd year in this career. I’ve been helping individuals, families and small businesses save money, spend money, start businesses, end careers, welcome babies, and say goodbye to loved ones. I’ve worked with well over two hundred clients and their families and coworkers, and they are all VERY different people. Some count all of their pennies and chart their savings and market performance, while others never look at it, to everything in between.

Overwhelmed Americans

One thing that most of our clients have in common is a feeling of being overwhelmed by the complexity of it all. Whenever I talk with clients, I’m the first to admit that the economic system that we are all trapped in is ridiculously convoluted. There is quite literally over a dozen types of accounts (as defined by the IRS) that any given individual might be able to use for savings. The tax laws are many and apply differently to nearly everyone, let alone if you experience changes from year-to-year. Aside from the legal restraints and rules, there are the enormous costs associated with keeping a roof over your head and paying for medical care. On top of all the have-to’s, there are the want-to’s. The cost of electronics alone, both monetarily and psychologically, is unprecedented in modern-day culture. Then consider the cost of housing in a safe neighborhood with good schools, vacations, and vehicles.

Americans deal with these challenges in different ways. Propel held a webinar in June 2020 that addressed the impact of COVID on families and small businesses. One of the topics we touched on was Money Personality. It’s important to acknowledge that a personality has a lot to do with how people perceive their financial situation.

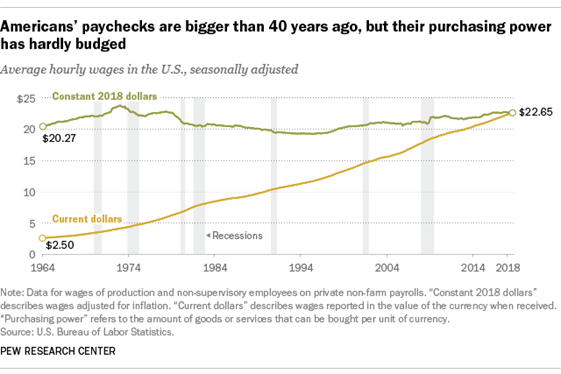

Stagnant Purchasing Power but Increased Choices

Despite the ever-growing list of things that we need and want, Americans have no more purchasing power than our parents did forty years ago when you consider inflation and the cost of living.

The upside is that many of us have a lot of choices. People are far more mobile now than they used to be as far as where they want to live and where they want to work. We also have a lot of resources available to us in terms of software and online information.

The upside is that many of us have a lot of choices. People are far more mobile now than they used to be as far as where they want to live and where they want to work. We also have a lot of resources available to us in terms of software and online information.

Regardless, many Americans, even those who are diligent savers, do not know how to plan for their financial futures. Some do not even try. There are those who are short-sighted or cannot appreciate the cost of their future selves. Others simply believe that planning is an exercise in futility (they will never have enough to retire anyway!), and they might as well enjoy the present. Psychologists say that many people think of their future selves as completely different people.

The Power of Planning

There is no denying that it takes work to become financially stable, but your income does not necessarily dictate your financial freedom. Some of our clients have never earned more than $40,000 per year in their lives, have no debt, and still have money in the bank. There are also those who earn ten times more than the average American and still have nothing to show for it. The magic ingredient is CONSISTENCY.

For those who lack consistency or for whom it isn’t quite enough, there are FINANCIAL ADVISORS. We work with people who possess varying levels of discipline and viewpoints and can help with an approach that makes sense for you. Propel has four intelligent, committed, bossy, and unemotional advisors to help you out! We know an awful lot about the various facets of Americans’ economic lives, including tax, estate planning, and investment management.

Meeting with a financial advisor when you retire is a must, but what if you had met with them 10 or 20 or 40 years earlier? Many people think financial advisors will only work with “rich” people. At Propel, we think that starting early and planning often are keys to successfully meeting your goals as your life changes. That’s why we work with people at ALL INCOME LEVELS.

The Financial Plan – In the Flesh (or on the Screen)

Since the start of the century, Americans have experienced three major economic downturns: 1) the dot.com bubble of 2000; 2) the Mortgage crisis of 2008; and 3) COVID in 2020. Despite major market upsets every ten years or so, today’s Americans are woefully unprepared. Why?

Prior generations in this country were able to rely on pensions. With the advent of 401(k) plans in 1978, the onus shifted away from employers and onto individuals to save for their futures. The consequence is that many people feel alone and overwhelmed by a complicated system. While we can only guess what everyone is thinking or not thinking, we expect that some of the reason for undersaving lies in the belief that saving for the future simply cannot be done.

But what if something could be done?

We at Propel argue that creating a plan and looking at the success of that plan once every 3 years (or more often depending on the changes in one’s life) will increase a person’s interest in participating in it, thus increasing its success even more.

When you sit down with your advisor, expect to spend between one and two hours having an initial conversation about your future self! Whether it takes one conversation or many, the end result is a written financial plan that is created from your own personal desires, concerns and concrete figures. We have created a simple financial plan template for you to see. In our example, we have made up a single woman named Responsible Jones. For simplicity’s sake, we’ve given her no spouse and no children, but a financial plan can include as many moving parts as you like.

| Responsible Jones is a single woman in her 40’s. She makes an adequate living and likes her home. However, Ms. Jones has no children, so she worries about who will care for her as she grows older and wants to be able to make choices about her finances, rather than be stuck with consequences. She has a 401(K), but she really has no idea what she owns or why it’s increased over the years. Ms. Jones wants to know if her social security and her 401(k) will be enough for her to feel financially stable as she moves toward retirement. |

The pages of interest to you may be:

• Plan Summary (pages 6-8 of the Plan): The first page summarizes the value of Ms. Jones’ assets and liabilities, the probability of success of her plan, and lists her goals, needs, and wants along with pertinent annual numbers. The second and third pages of the Summary shows her investment allocation and discusses her social security options.

• Personal Information, Goals, Expectations and Concerns (pages 9-11 of the Plan): These pages are created by you as you work with one of our advisors to talk about what is important to you, what is worrying you, and what you are hoping to achieve. You even get to rate them based on their importance. This section really gives our clients the chance to choose what they want to focus on, and it gives us insight into their risk tolerances.

• Net Worth Detail (page 12 of the Plan): This section puts all of your assets and liabilities on one page for you to see.

• Risk Assessment (page 13 of the Plan): This page consolidates all the notes that your advisor has taken based on your conversation(s). Clients often learn that their risk tolerance is different than what they thought.

• Results (pages 14-16 of the Plan): We can have a lot of fun with these pages, which allow us to choose a variety of scenarios and compare what they might look like and how they might impact your priorities and savings disciplines. In Ms. Jones’ Plan, we didn’t bother to create multiple scenarios, but oftentimes clients are trying to make a choice or two or three, and this report helps you to do that.

Individual Plans for Every Purpose

While Ms. Jones’ Plan is very simple and is focused solely on retirement, we have a lot of tools at our disposal to make it as comprehensive as you like. You can plan for college savings, vacations, a home purchase, working after retirement from your primary job, health care needs, etc.

Even if you create a Plan that you are happy with, life changes. Should you experience a sudden influx of money from an inheritance or a job promotion or should you suffer from a market downturn, job loss or major health setback, the first Plan you created can be modified to address these changes going forward without having to start all over.

Just as your Plan is very specific to you, so are our fees. Most simple plans are charged a flat $300 with additional charges for additional scenarios and updates. We are happy to work with you on a one-time fee or a rolling payment plan so that you can stay on top of your Plan no matter what life throws at you. All of us at Propel use these Plans and find them extremely helpful.

We encourage you to reach out to your Advisor and create a Plan, even if it’s just a simple one to get started. It gets you thinking differently about your money and how it serves you. We look forward to helping you get to know yourself and your finances a little bit better.